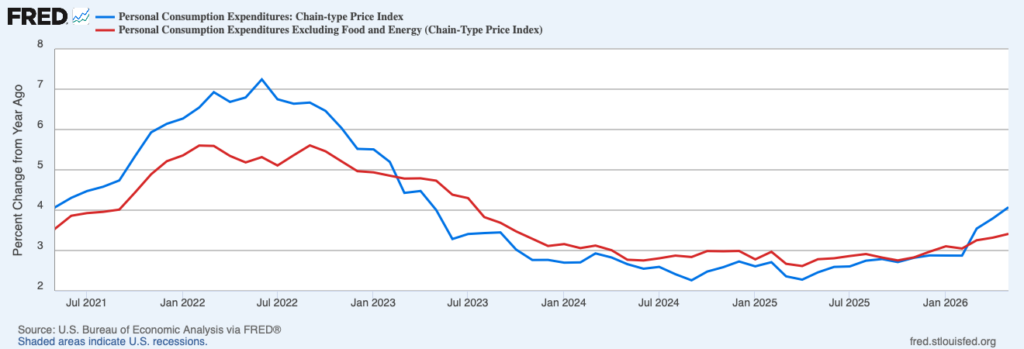

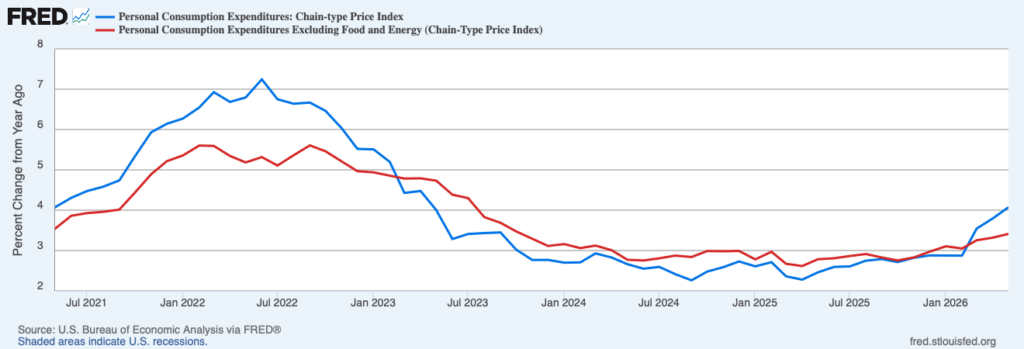

Federal Reserve Chairman Kevin Warsh has inherited a major inflation problem. Rather than abating as the conflict in the Middle East winds down, the latest data from the Bureau of Economic Analysis reveal inflation has gotten worse. The Personal Consumption Expenditures Price Index (PCEPI), the Federal Reserve’s preferred measure of inflation, grew at an annualized rate of 5.5 percent in May 2026, up from 5.0 percent in the prior month. The PCEPI grew at an annualized rate of 5.3 percent over the last six months and 4.1 percent over the last year.

Core inflation, which excludes food and energy prices and is thought to be a better gauge of the underlying rate of inflation, also ticked up. Core PCEPI grew at an annualized rate of 3.9 percent in May 2026, up from 3.0 in the prior month. It grew at an annualized rate of 4.1 percent over the last six months and 3.4 percent over the last year.

Constrained energy supplies associated with the Middle East conflict are partly to blame. Energy prices were 24.3 percent higher in May than they had been a year earlier. But that’s only part of the story, as greater price pressure appears to be widespread. Goods prices, which grew at an average annualized rate of -0.1 percent over the five years just prior to the pandemic, have grown 4.8 percent over the last year. Services prices have grown 3.8 percent over the last year, compared with 2.3 percent over the five years just prior to the pandemic.

Persistent, high inflation is a problem for the Fed, particularly when it is widespread. And the newly appointed Fed Chairman has vowed to tackle that problem.

“We recognize that inflation has been running well ahead of the Fed’s longstated inflation goal of two percent,” Warsh told reporters at the post-meeting press conference earlier this month. “That’s been going on for more than five years. […] But the recent past need not be prologue.” He said “members of the FOMC are unambiguous and unanimous” in declaring that they “will deliver price stability.”

The Summary of Economic Projections, released in conjunction with this month’s meeting, offers more tough talk from FOMC members. The median member (excluding Warsh, who did not submit a projection) thought the federal funds rate target range would be 25 basis points higher by year-end. Five members projected it would be 50 basis points higher and one projected it will be 75 basis points higher.

Back in March, all 19 members said they thought the federal funds rate would be within or below the current 3.5 to 3.75 percent target range at the end of 2026.

The change in tone at the Fed is noteworthy. But FOMC members still appear to be behind the curve. In June, the median FOMC member revised up their inflation projection for the year, from 2.7 percent to 3.6 percent. Given the inflation realized through May, however, the latest projection implies prices will grow at an average annualized rate of just 2.2 percent over the next seven months. That seems unlikely.

Despite the undue optimism from FOMC members, market participants seem to have accepted the tough talk at face value. Indeed, they expect the FOMC will deliver a bigger rate hike than was projected. According to the CME Group, there is a 39.9 percent chance that the federal funds rate will be 25 basis points higher following the December 2026 meeting; a 30.5 percent chance they will be 50 basis points higher; and a 10.9 percent chance they will be more than 50 basis points higher. In other words, market participants expect FOMC members will soon realize inflation is worse than they thought and adjust policy accordingly.

The FOMC’s tougher tone has bolstered its credibility. But tough talk becomes cheap talk if the FOMC does not follow through. Assuming inflation continues to run above the median FOMC member’s projection, Warsh and his colleagues will have to revise their views quickly and act accordingly. Market participants believe the FOMC will deliver, for now. Warsh’s first major test is to prove them right.