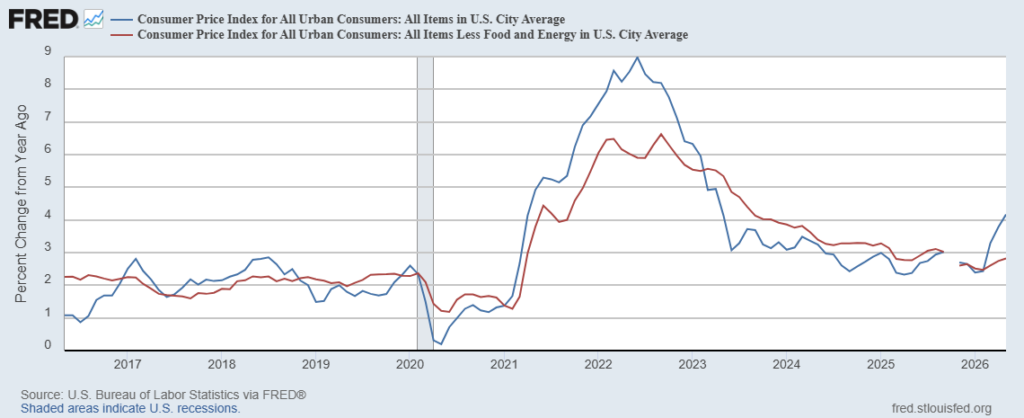

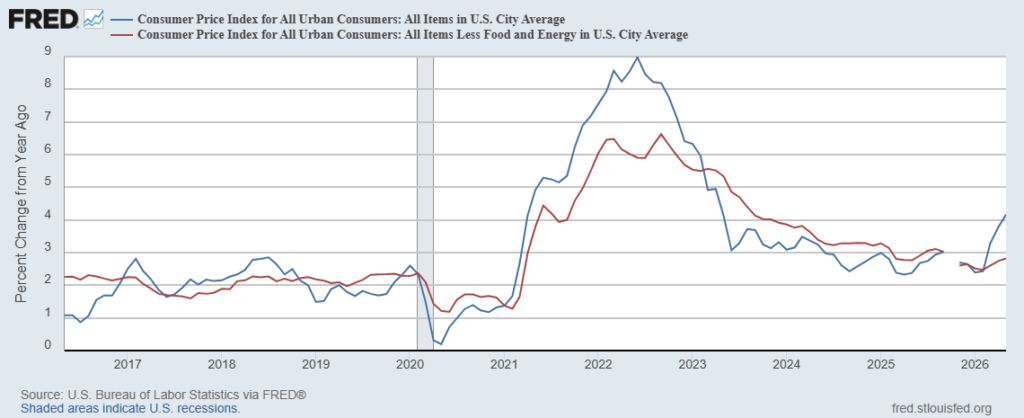

Inflation remained elevated in May, the Bureau of Labor Statistics (BLS) reported yesterday. The Consumer Price Index (CPI) rose 0.5 percent last month, down slightly from 0.6 percent in April. But on a year-over-year basis, headline inflation climbed again, rising to 4.2 percent from 3.8 percent — the fourth straight monthly increase in the annual rate and the highest reading in more than a year.

Core inflation told a more reassuring story. Excluding volatile food and energy prices, CPI rose just 0.2 percent in May, half the 0.4 percent pace recorded in April. On a year-over-year basis, core inflation ticked up only slightly, to 2.9 percent from 2.8 percent.

As in March and April, the gap between headline and core inflation came down to energy. The energy index rose 3.9 percent in May — after climbing 3.8 percent in April and 10.9 percent in March — and, according to the BLS, “accounted for over sixty percent of the monthly all items increase.” Gasoline prices rose 7.0 percent over the month and are now up 40.5 percent over the past year, while the broader energy index is up 23.5 percent, reflecting the cumulative effect of the oil shock tied to the conflict involving Iran and the disruption to shipping through the Strait of Hormuz. Outside of energy, the monthly gains were comparatively muted. Shelter, which accounts for about one-third of the index, rose 0.3 percent in May and is up 3.4 percent over the past year, while food prices rose 0.2 percent over the month and 3.1 percent over the year.

Within the core, the big moves largely canceled out. Airline fares jumped 2.7 percent in May and are up 26.7 percent over the past year, while motor vehicle insurance fell 1.7 percent and is down 2.0 percent from a year ago. With little movement elsewhere, core inflation slowed to 0.2 percent even as the headline figure stayed elevated.

In short, the categories excluded from core — energy above all — pulled the overall index up, while underlying price pressures eased.

The three-month trend underscores how much of the recent acceleration is an energy story. From March through May, headline CPI averaged about 0.67 percent per month, equivalent to roughly an 8 percent annual rate — well above the 4.2 percent year-over-year figure. But that pace is almost entirely a product of the energy spike. Strip out food and energy, and the picture changes sharply: core CPI rose 0.2 percent in March, 0.4 percent in April, and 0.2 percent in May, an average of roughly 0.27 percent per month, or about a 3.3 percent annual rate. That is only modestly above the 2.9 percent year-over-year core pace, and well below what the headline trend implies.

Although the Federal Reserve officially targets the personal consumption expenditures price index (PCEPI), CPI data remain a timely and relevant gauge for policymakers, since the two measures generally track one another closely. According to the CME Group’s FedWatch tool, markets are assigning a 98.4 percent probability that the Fed will hold rates steady at its meeting next week.

The labor market data give policymakers no reason to ease in the face of that elevated inflation. Employers added 172,000 jobs in May, and the unemployment rate held at 4.3 percent, the BLS reported last Friday. The Bureau also revised March and April payrolls up by a combined 93,000, lifting April’s gain to 179,000 from the 115,000 first reported. With labor-force growth held down by an aging population and reduced immigration, the participation rate steady at 61.8 percent, and the employment-population ratio little changed at 59.2 percent, the economy appears to be near full employment — a setting in which even modest monthly job gains no longer signal a weakening economy.

Taken together, the May data point to something more than a passing energy shock. Above-target inflation that keeps drifting higher, alongside a labor market near full employment, is hard to square with the view that oil alone is to blame. Supply shocks change relative prices; they do not, by themselves, push the overall price level up year after year. That requires excess nominal spending, which grew 5.9 percent over the year through the first quarter — well above the roughly 4 percent pace that prevailed before the pandemic. By that standard, the recent run of inflation looks less like a temporary disruption and more like a monetary phenomenon.

Governor Christopher Waller, a leading voice on the FOMC, made a similar case in a recent speech. With the labor market stable and inflation elevated, he said he would drop the “easing bias” from the Fed’s policy statement and hold the rate steady, warning that price pressures were broadening beyond energy — about half of consumer prices have risen 3 percent or more this year, a historically large share. He also noted that, with workforce growth near zero, “little or no job creation is now consistent with a stable labor market,” and he declined to rule out a rate increase if inflation failed to recede.

The May CPI report, even with its softer core reading, fits that diagnosis. The single-month deceleration in core prices is welcome, but it does not change the broader picture: inflation remains above the Fed’s two-percent target, and it is being driven by demand that is still running too hot. For now, the case for cutting rates is weak — and if nominal spending fails to slow, the harder question facing the Fed may not be when to cut, but whether it will have to move in the other direction.