Not long ago, the notion of trillions belonged either to the furthest cosmic reaches of the universe or the submicroscopic world of atoms. These numbers describe galaxies in the observable universe, roughly two trillion, or, at the opposite extreme, the picosecond — one trillionth of a second — is used to measure molecular motion and chemical reactions. Until recently, magnitudes denominated in trillions were almost entirely confined to the theoretical hinterlands of astronomy, physics, and schoolyard exaggeration.

Today, trillion-dollar quantities have become commonplace in economic and financial life. At least 12 American companies boast trillion-dollar market capitalizations, with Apple approaching $5 trillion. BlackRock now manages more than $15 trillion in assets. The largest technology firms, cumulatively, measure their investments in the trillions as they build data centers, semiconductor capacity, and power systems on an unprecedented scale. SpaceX’s 2026 initial public offering valued the company at more than $1.7 trillion, and its subsequent surge briefly pushed Elon Musk’s paper wealth above $1 trillion.

Billionistan opened its gates in 1901, when JP Morgan assembled US Steel into the world’s first billion-dollar corporation. Perhaps it surrendered statehood on January 13, 2016, the day Powerball offered the first billion-dollar lottery jackpot. After ten more, Billionistan moved from a numerical destination to a waypoint. We now inhabit Trillionistan.

Governments, unsurprisingly, were early movers; they frequently are. Trillion-dollar economic figures first appeared during the great hyperinflations of the twentieth century. In the United States, the national debt crossed $1 trillion in October 1981, inaugurating an era in which ever-larger fiscal quantities gradually lost their capacity to shock. Annual deficits now exceed the entire national debt of 45 years ago, while America’s current indebtedness — as measured by the fiscal gap — extends into the hundreds of trillions.

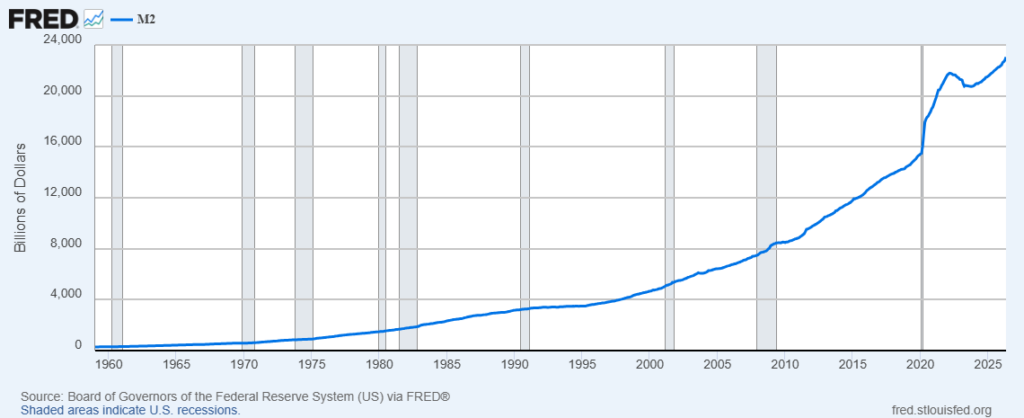

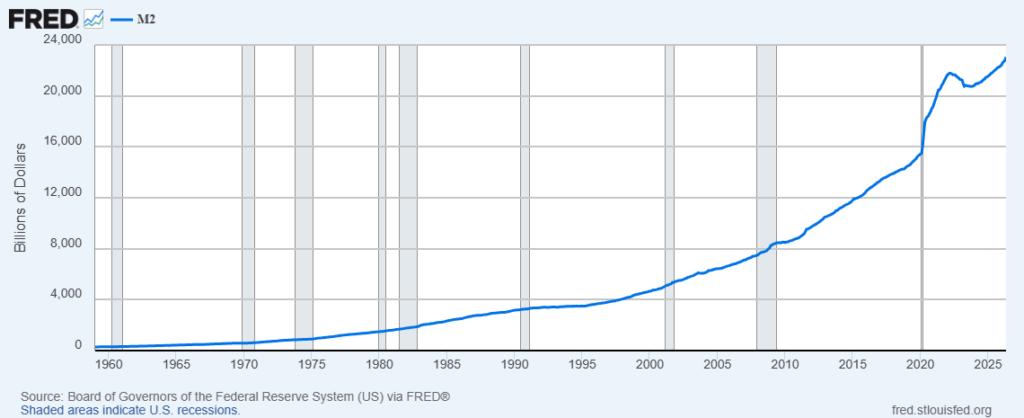

Public finance is only one province of Trillionistan. The larger phenomenon is the steady upward drift of nominal magnitudes — and our tendency to mistake financial scale for real, truly productive achievement. Prices rise, credit and money supplies balloon, economies grow, markets deepen, and expected future earnings are capitalized across ever-longer horizons. Each process quietly extends the number of zeroes layered onto economic life.

Inflation is plainly part of the explanation. A dollar simply buys far less than it once did. Even if nothing real changed — if no new factories were built, no technologies discovered, and no improvement in living standards achieved — the same collection of assets would be priced higher over time as each dollar lost purchasing power. Nominal dollar records are easier to achieve than real value-driven ones.

But inflation alone cannot explain Trillionistan. The economy has also become larger, richer, more technologically sophisticated, and more global. Companies now serve billions of customers, software scales almost without cost, and intellectual property can generate extraordinary returns worldwide. Genuine wealth creation and monetary depreciation are operating simultaneously, both enlarging the nominal quantities around us. But it’s difficult for most observers to distinguish between a trillion dollars of productive assets, a trillion dollars of debt, a trillion-dollar market cap, a trillion-dollar spending bill, and a trillion dollars of future pension liabilities.

Sound economics cautions against confusing abstract money prices with the goods, services, productive capacities, and human satisfactions to which those prices refer. Additional wealth is not created merely because accountants add zeros to balance sheets, central banks expand the money supply, or financial assets are quoted at higher prices. Yet neither are such price changes meaningless. Money is a messenger: prices may reflect changes in scarcity, expected earnings, risk, preferences, credit conditions, monetary supply, or some combination of them. Wealth is created when entrepreneurs discover more valuable ways to arrange scarce resources, including capital and labor, to satisfy human wants. Market prices signal judgments about those uses, but they are not themselves the value being created.

Viewed through that lens, a trillion-dollar company is less alarming, and perhaps more inspiring. A trillion-dollar market capitalization is not a warehouse containing a trillion dollars; it is the market’s continuously revised estimate of future earning power (see the price trend in SpaceX since the IPO for confirmation of that phenomenon). Stock prices condense millions of judgments about technology, competition, consumer demand, production costs, and risk into a single signal of likely value. That estimate — whether it proves accurate or wildly optimistic — is a wager, a priced forecast of the future, rather than an inventory of existing riches.

Like the trillions now being committed to AI infrastructure, some investments will transform productivity; others will become expensive monuments to extrapolation. Entrepreneurship has always involved speculation. The more important question is whether monetary policy choices have the effect of systematically warping entrepreneurial judgment and promoting malinvestment. Persistently easy credit and artificially suppressed interest rates do more than raise prices generally. They encourage longer-duration projects, inflate the present value of distant earnings, and allow financial valuations to outrun the economy’s underlying productive capacity.

Certainly not every trillion dollar valuation is a bubble. Monetary distortion and genuine innovation frequently coexist. Railroads truly transformed nineteenth-century Millionistan — the impressive Mohawk and Hudson Railroad was built for just $600,000 — though many fortunes disappeared in speculative railroad manias. The internet continued to power our economy well after the collapse of the dot-com bubble. Artificial intelligence may likewise reshape civilization while simultaneously destroying vast quantities of invested capital. Entrepreneurial ventures, especially at the cutting edge of technology, are entrepreneurial wagers. Profit and loss exist precisely because no one knows the outcome beforehand.

Life in Trillionistan has rewired our perceptions. Large numbers anesthetize. A million dollars once represented unimaginable wealth; a billion eventually replaced it; today even the billion is becoming commonplace. As each numerical frontier becomes familiar, it commands less wonder and less scrutiny. We experience reflexive suspicion of individuals who command great fortunes, but slip into complacency toward inflation, debt, and public liabilities. In both cases, the magnitude obscures the institution that produced it.

Not all trillions are created equal. A trillion accumulated through entrepreneurial discovery differs fundamentally from a trillion generated through monetary expansion, leverage, or habitual political can-kicking. Most modern trillions contain elements of both: genuine productive achievement expressed through a steadily depreciating unit of account. The trillion has migrated from cosmology and quantum mechanics into ordinary economic discourse because the economy has genuinely grown, but also because the monetary unit has contracted precipitously.

The important question, then, is not whether another company, fortune, industry, or balance sheet will cross the trillion-dollar threshold. Many will. The more interesting and relevant question is what kind of trillion it will be: one representing genuine wealth creation, one reflecting the capitalization of future possibilities, one inflated by monetary expansion, or some unstable mixture of all three. In Trillionistan, the zeros hint at the scale, but they do not tell us the actual story. And even as we acclimate ourselves to the trillion, the foundations of Quadrillionistan are quietly being laid.