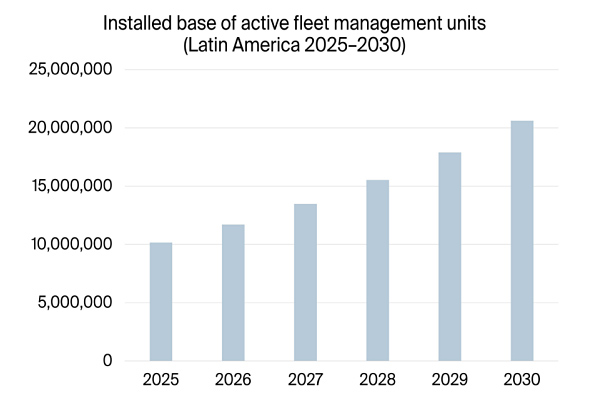

Berg Insight expects the installed base of fleet management systems in Latin America to reach 20.6 million units by 2030, pointing to a larger addressable market for telematics connectivity, platforms and lifecycle services across the region.

Fleet management in Latin America is often discussed in terms of hardware adoption, but the more important signal for the IoT ecosystem is the size of the active installed base. Devices already deployed in vehicles generate recurring demand for cellular connectivity, cloud platforms, integrations, support, upgrades and data-driven services long after the initial sale.

That is why Berg Insight’s latest forecast matters. The research firm says the installed base of fleet management systems in Latin America will reach 20.6 million units by 2030. The figure does not describe a one-off shipment opportunity; it points to a large operational footprint of connected vehicles that will need to be managed, billed, secured and integrated into business processes over time.

A market signal, not a product announcement

What makes this announcement distinct from the typical IoT industry release is its focus on installed systems rather than a new device, connectivity offer or platform feature. In telematics, this distinction is important. Shipments can indicate short-term sales momentum, but installed base data is more directly tied to recurring service revenues and operational complexity.

For connectivity providers, 20.6 million active fleet management units imply a substantial base of SIMs, data plans and roaming or multi-network arrangements. For platform providers, the number points to continuing demand for device onboarding, vehicle data normalization, maintenance workflows, driver behavior analytics and customer support. For enterprises operating fleets, it suggests that telematics is becoming a mainstream operational layer rather than a peripheral technology purchase.

The forecast also underlines the specific nature of fleet IoT in Latin America. Fleet management systems are not simply connected gadgets attached to vehicles; they sit at the intersection of logistics, fuel costs, security, maintenance, compliance and driver productivity. As adoption expands, the challenge shifts from proving the value of tracking to integrating vehicle data into dispatch, insurance, finance, maintenance and customer-facing systems.

Why the installed base metric matters

A concrete implication of Berg Insight’s forecast is that the region’s telematics market will increasingly be shaped by replacement cycles and service continuity, not only by first-time deployments. Once a fleet management unit is in the field, the commercial relationship depends on keeping connectivity active, firmware maintained, dashboards usable and integrations reliable. That creates a different set of priorities for IoT vendors than a pure hardware sales model.

OEMs and device manufacturers can read the forecast as evidence of a growing market for robust in-vehicle hardware, but the larger opportunity is tied to long service lives and remote manageability. In practice, this makes provisioning, diagnostics and support capabilities nearly as important as the device itself. Connectivity providers, meanwhile, need to support large numbers of mobile assets that may operate across regions, networks and coverage conditions.

System integrators are likely to see demand around integration rather than simple installation. As fleets add more connected vehicles, customers will need telematics data linked to enterprise software, routing tools, maintenance systems and reporting environments. The complexity is less about connecting one vehicle and more about making thousands of vehicle data points usable across different departments.

For industrial players and logistics operators, a larger installed base also raises expectations. Once competitors have visibility into vehicle location, utilization and maintenance status, telematics becomes part of the baseline for operational efficiency. The technology does not remove regional infrastructure constraints, but it gives operators better data to manage them.

Broader implications for IoT in the region

The Latin American fleet management market is a useful indicator for the wider IoT sector because it combines mobility, recurring connectivity and business-critical operations. Unlike some consumer IoT categories, fleet telematics typically has a direct operational rationale: reducing downtime, improving asset utilization, supporting driver management and increasing visibility over distributed operations.

Berg Insight’s 2030 forecast therefore points to more than growth in one vertical. It suggests that Latin America will represent a significant base of connected mobile assets requiring long-term IoT service delivery. The companies best positioned to benefit will not necessarily be those selling the most hardware, but those able to keep devices connected, data usable and services reliable across the full lifecycle of the fleet deployment.

The post Berg Insight Forecasts 20.6 Million Fleet Management Systems in Latin America by 2030 appeared first on IoT Business News.