Berg Insight estimates that cellular IoT module shipments reached 612 million units in 2025, while revenues rose to US$5.6 billion. The figures point to a market recovery, but also to growing pressure on module pricing and component costs.

For cellular IoT device makers, 2025 was not simply a return-to-growth year. It was a reminder that volume recovery and value recovery are no longer moving in lockstep across the module supply chain.

New data from Berg Insight shows that annual shipments of cellular IoT modules reached 612 million units in 2025, up 33 percent from the previous year. Revenues increased by 19 percent to US$5.6 billion. The figures exclude automotive NAD modules, which are typically treated as a separate segment because of their qualification requirements, supply chains and pricing dynamics.

That gap between unit growth and revenue growth is one of the more important takeaways from the report. Based on Berg Insight’s figures, average revenue per shipped module declined year-on-year, even as the market expanded sharply in volume terms. For OEMs and connectivity hardware vendors, this points to a market where demand has recovered, but pricing power remains uneven.

A recovery shaped by inventory correction and local policy

Berg Insight attributes the rebound to stronger demand across all major regions after a weaker period caused largely by elevated customer inventories. In practical terms, this suggests that part of the 2025 surge reflects the clearing of excess stock in the channel rather than only new end-market expansion.

The report also highlights additional momentum from local policies in selected countries, including Spain and China. That detail matters because cellular IoT module demand is often driven as much by regulatory or public-sector requirements as by organic enterprise digitisation. Smart metering, payments, utilities, public infrastructure and compliance-led device refresh cycles can all create concentrated demand for specific module categories, even when broader enterprise IoT spending remains cautious.

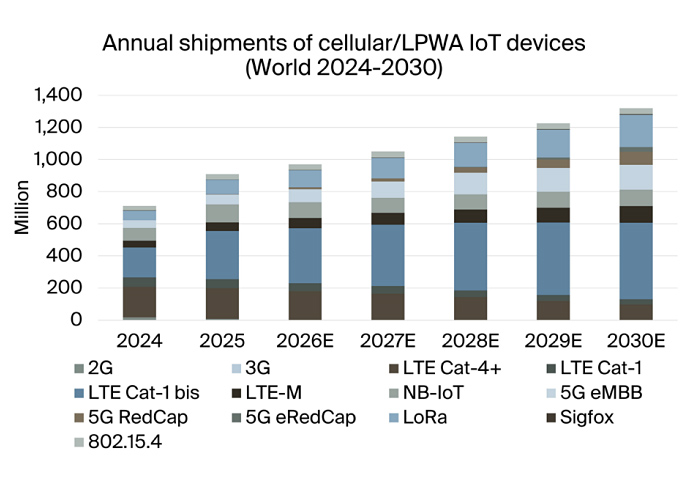

Berg Insight forecasts cellular IoT module shipments to grow at a compound annual growth rate of 7 percent through 2030, reaching 878 million units. Compared with the 33 percent jump recorded in 2025, that outlook implies a normalisation of growth after the post-inventory rebound.

Why this is not just another growth headline

The distinctive feature of this market update is the combination of renewed demand with a new cost-side constraint coming from outside the traditional IoT ecosystem. Berg Insight notes that the growth trend has continued into 2026, but that memory pricing has become a mounting challenge as memory manufacturers allocate more production capacity to high-bandwidth memory for AI servers and data centre infrastructure.

That creates an unusual cross-market pressure point. Cellular IoT modules are not competing with AI servers in terms of end application, but they are indirectly exposed through shared semiconductor supply chains. The report indicates that the immediate effect has been price pressure rather than outright shortages, with 5G modules most exposed because they typically contain more memory and rely on more advanced DRAM technologies. Legacy-memory-based 4G LTE modules are less affected, although Berg Insight says few products are fully insulated.

The operational consequence is clear: module pricing is becoming less static. Vendors are introducing periodic price reviews and contractual mechanisms to manage component cost volatility. For OEMs and system integrators, that can complicate long-cycle product planning, especially where device business cases depend on stable bill-of-materials costs over multi-year deployments.

Vendor concentration remains high

The competitive structure of the module market remains concentrated. Berg Insight reports that Quectel, Fibocom, Telit Cinterion, MeiG and China Mobile IoT together accounted for 73 percent of cellular IoT module revenues in 2025.

Volume leadership, however, is strongly shaped by China’s domestic market. Quectel, China Mobile IoT, Sunsea AIoT, Lierda and Fibocom are identified as the leading vendors by volume, benefiting from large-scale domestic demand. Berg Insight also notes the rapid emergence of ZXInfoTek, particularly in POS terminals, a segment where connectivity modules are closely tied to payment device refresh and deployment cycles.

The chipset picture reinforces the same regional dynamic. Berg Insight estimates that cellular IoT chipset shipments, excluding automotive-grade products, reached 706 million units in 2025. ASR Microelectronics, Qualcomm, Eigencomm, UNISOC, Xinyi and MediaTek were the main suppliers. China-based chipset vendors had a strong year in volume terms, with ASR, Eigencomm and Xinyi reporting solid growth in LTE Cat-1 bis and NB-IoT. Qualcomm retained a substantial position in LTE-M, high-end 4G LTE and 5G eMBB chipsets.

For connectivity providers and enterprises, the report underscores a more fragmented planning environment. Low-cost cellular IoT categories continue to scale, 5G module economics are more exposed to memory pricing, and vendor choice increasingly depends on the target application, geography and technology tier. The market is growing again, but the economics behind that growth are becoming more complex.

The post Cellular IoT Module Market Returns to Double-Digit Growth as Revenues Reach $5.6 Billion appeared first on IoT Business News.