When Britain voted to leave the European Union (EU) on June 23, 2016, there were dire predictions for its economy. Prime Minister David Cameron and Chancellor George Osborne cited a Treasury analysis forecasting that “a vote to leave will push our economy into a recession that would knock 3.6 percent off GDP and, over two years, put hundreds of thousands of people out of work right across the country, compared to the forecast for continued growth if we vote to remain in the EU.”

This doomsday scenario did not come to pass. Britain’s economy stubbornly refused to collapse after the referendum, and when it did, it did so for the same reason every other economy did: COVID-19.

If we compare the British economy’s performance pre- and post-Brexit with that of its peers in the G7, it is hard to see the prophesied economic meltdown.

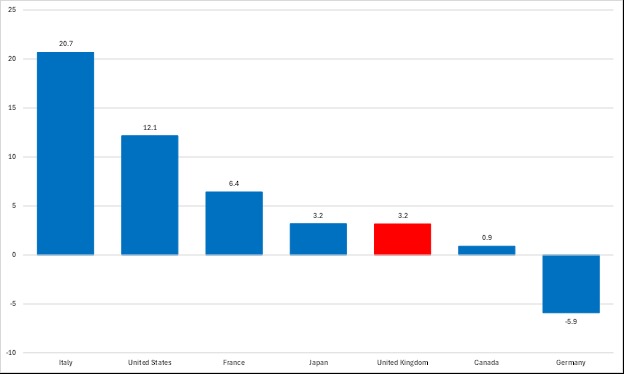

Figure 1 (see below) shows the percentage point change in per capita GDP growth — the measure that really matters for economic welfare — among the G7 in the pre- and post-Brexit periods. We see that Britain’s per capita GDP growth was 3.2 percentage points higher in the period after Brexit — 2016 to 2025 — than in the period before — 2007 to 2016 — a better performance than in two other G7 countries, Canada and Germany, and on a par with a third, Japan; hardly an economic catastrophe.

Figure 1: Percentage point change in real per capita GDP growth, 2007 to 2016/2016 to 2025 (Annual levels, Calendar and seasonally adjusted, US dollars per person, PPP converted, 2020)

Even so, some researchers argue that there was a significant economic hit from Brexit. Economists Nicholas Bloom, Philip Bunn, Paul Mizen, Pawel Smietanka, and Gregory Thwaites with the National Bureau of Economic Research (NBER) recently estimated that by 2025, Brexit had reduced UK GDP by six and eight percent, relative to 2016.

There are reasons to doubt this.

First, the NBER paper, like others, does not compare Britain’s post-Brexit economic performance to the post-Brexit performance of these other countries but to the post-Brexit performance of a constructed “doppelgänger,” which, as economist Julian Jessop notes, is rather puzzlingly assembled. The eight countries it is built from include neither France nor Germany, but does include two Baltic states and the United States. It is hard to see the rationale for these choices.

Second, it ascribes all of Britain’s underperformance relative to the doppelgänger to Brexit. Yet the G7 member with the steepest fall in both per capita and total GDP growth pre- and post-Brexit is Germany, which remained in the EU. Much of its dismal economic performance in recent years can be ascribed to its “green energy” policies, but if we must account for factors besides EU membership when assessing Germany’s underperformance, why do we not do so for Britain?

Under the post-Brexit Conservatives and Labour since 2024, the British economy has been strangled with ever-higher taxes and regulatory burdens, which would have hampered its growth even if the country had voted to remain in the EU. This must be accounted for when assessing the economic impact of Brexit.

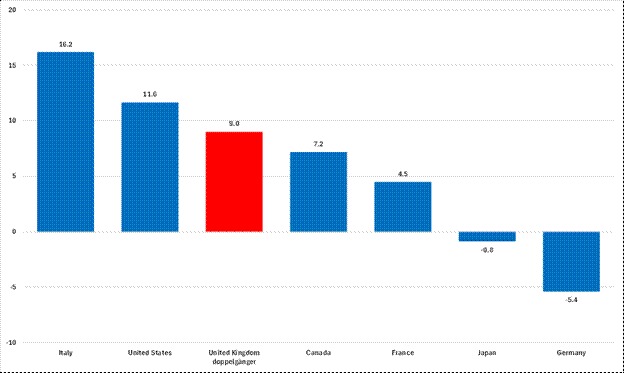

These methodological problems perhaps account for the striking results. If the British economy really had grown by another seven percent, it would have climbed from the 4th fastest growing G7 economy in the period 2007 to 2016 to third fastest in the period 2016 to 2025, which is certainly possible. But, as Figure 2 shows, the performance posited by the NBER economists implies that, if Britain had remained in the EU, its GDP growth in the ten years after 2016 would have been 9.0 percentage points higher than in the ten years before 2016. This would be an improvement better than all but two other G7 countries: Italy, whose economy, from 2016 to 2025, was recovering from a collapse in GDP of 6.7 percent between 2007 and 2016, and the United States, which is the G7’s leader in terms of GDP growth.

Figure 2: Percentage point change in real GDP growth rate from 2007/2016 to 2016/2025 (Growth rate, period on period, Chain linked volume, Calendar and seasonally adjusted)

Is this likely? Was the British economy really poised for such a robust performance in 2016? Those who recall the jeremiads about the economic damage wrought by the Cameron government’s “austerity” will be surprised.

Why did Brexit fail to live down to the economic warnings?

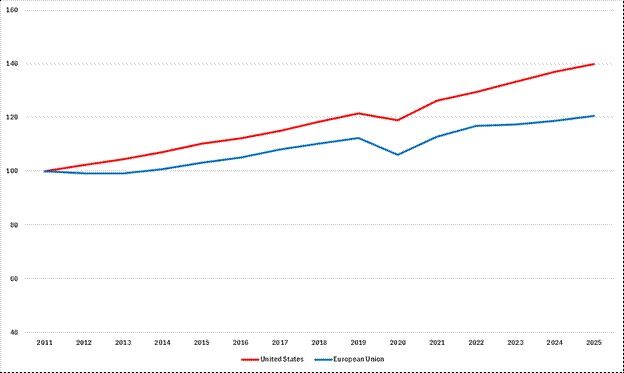

First, the EU is an economic laggard. As Figure 3 shows, since 2011, the EU’s economy has grown by 20.6 percent while the US economy — the second biggest destination for British exports after the EU in 2016 — grew by 39.9 percent, nearly double the rate.

Figure 3: Real GDP growth (Growth rate, period on period, Chain linked volume, Calendar and seasonally adjusted)

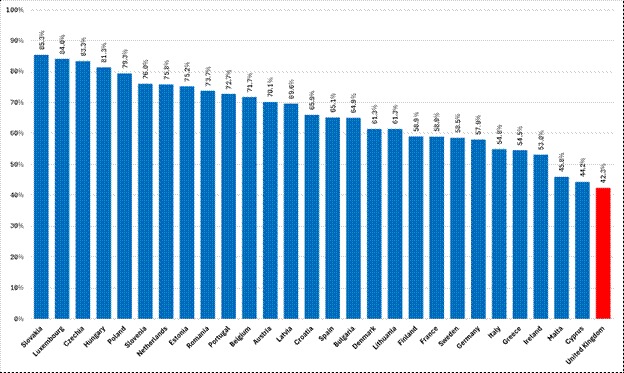

Second, Britain’s economy was one of the least reliant on its EU colleagues. As Figure 4 shows, in 2015, just 42.3 percent of British exports went to the EU, a share lower than in each of the 27 other members. This is partly because, as Luis Garicano, a former member of the European Parliament, noted recently, the “Single Market” is largely a myth.

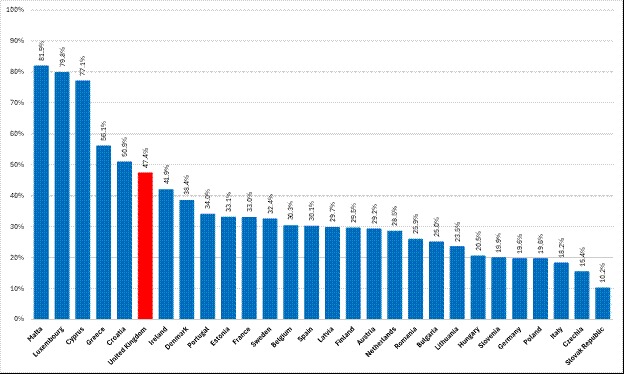

“The IMF puts the hidden cost of trading goods inside the EU at the equivalent of a 45 percent tariff,” he writes. This is especially so for services where “the figure climbs to 110 percent, higher than Trump’s ‘Liberation Day’ tariffs on Chinese imports.” This is a particular issue for Britain, where, as Figure 5 shows, services accounted for a greater share of exports in 2015 than in 22 of the 27 other EU countries.

Figure 4: Share of exports to other EU Members, 2015

Figure 5: Services as a share of total exports, 2015

A decade on, these facts are little changed, and hopes that Britain’s economy can be boosted by closer ties with — or even rejoining — the EU are doomed to disappointment. As with other “exits,” whether the British economy flourishes will largely depend on what happens in Britain. And if you wrote in 2016 that “we doubt that Britain’s long-term economic outlook hinges on [EU membership],” you might be feeling rather vindicated.

But perhaps this is missing the point. For most, Brexit was never really about economics at all. That was merely a proxy for the debate people wanted to have but were afraid to openly; the more elemental one of identity. In the decade since Brexit, they have become less afraid.