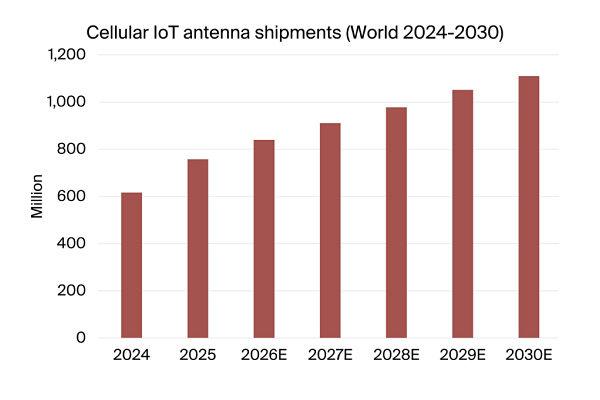

Berg Insight says cellular IoT antenna shipments rose 23% in 2025. The milestone is a reminder that as LPWAN and 5G-era use cases expand, antenna design and sourcing are becoming a volume hardware topic again—not just an RF detail left to late-stage product engineering.

Connectivity is often discussed in terms of silicon roadmaps, coverage maps and subscription economics. But at the point where IoT deployments move from pilots to industrial scale, the physical layer has a habit of reasserting itself. Antennas—usually treated as a small line item in a bill of materials—can become a defining constraint when device makers must ship millions of units while keeping certification risk, supply continuity and in-field performance under control.

That backdrop matters for a new data point from market research firm Berg Insight: cellular IoT antenna shipments grew 23 percent in 2025, reaching 757 million units. For an industry that has spent the past few years focused on module availability, LTE-M/NB-IoT footprint expansion and the early contours of 5G for IoT, the number is a tangible indicator that the hardware side of cellular IoT is now operating at consumer-electronics-like volumes in many segments.

Why antenna data offers a clearer view of IoT adoption

Unlike module shipment figures—which often bundle multiple radio variants and can be hard to translate into deployment reality—antenna shipments are tightly coupled to physical devices. A cellular IoT antenna is rarely purchased “just in case”; it is usually selected for a specific product, enclosure, mounting method and regulatory path. In other words, antenna volumes can serve as a proxy for how many cellular-connected endpoints are actually being built across categories.

The differentiation in Berg Insight’s announcement is precisely this focus on a component that sits at the intersection of RF engineering and manufacturing operations. Many industry updates track network or chipset trends. Antenna shipment growth, by contrast, points to the less glamorous work of turning connectivity into repeatable hardware designs: matching radiating elements to real-world installation conditions, navigating detuning effects from plastics or metal housings, and maintaining consistent performance across manufacturing tolerances. Those issues do not disappear with more advanced cellular standards; they often become harder as devices shrink, add bands, or need to coexist with GNSS, Wi-Fi or Bluetooth inside the same enclosure.

What 757 million shipments implies for the ecosystem

A 23 percent year-on-year increase to 757 million units suggests that cellular IoT is broadening beyond a handful of high-volume verticals and into a wider base of “quiet scale” products: devices that don’t attract headlines individually but add up across utilities, industrial monitoring, security, logistics and embedded OEM designs.

It also implies a shift in where risk sits. At lower volumes, antenna selection mistakes can be painful but containable. At the volumes Berg Insight is pointing to, small design choices—connector types, cable routing, adhesive mounting, tuning methodology, and supplier qualification—become recurring operational issues. The practical consequence is that antenna sourcing and validation increasingly look like strategic supply chain decisions rather than late-stage RF checkboxes.

There’s another operational insight embedded in antenna growth: as more device makers standardise on embedded or compact designs, external antennas are not simply “accessories.” They are often the mechanism that lets an OEM use the same core electronics across multiple geographies, installation types and enclosure variants. Rising antenna shipments can therefore reflect product-line strategies aimed at reuse and faster SKU expansion—without changing the modem or baseband design each time.

Implications for OEMs, integrators and connectivity providers

For OEMs, Berg Insight’s figure is a reminder that antenna engineering deserves earlier involvement in product definition, especially for devices expected to ship at scale. Mechanical decisions—materials, mounting positions, cable lengths, and grounding—can lock in RF outcomes long before a lab test. If cellular IoT is now shipping hundreds of millions of antennas annually, competitive differentiation can come from getting these fundamentals right consistently across product generations.

System integrators and solution providers should read the growth as a signal that “RF performance in the field” will remain a source of deployment variability. As projects scale, variability becomes an operational cost: more truck rolls, longer commissioning, and higher rates of “connectivity issues” that are actually antenna placement or enclosure interactions. Antenna-aware installation guidelines and acceptance testing can become a measurable part of project quality.

Connectivity providers, meanwhile, may find that antenna-related performance issues increasingly affect perceived network quality. When endpoints are deployed in basements, behind metal panels, or on moving assets, the difference between a good and mediocre antenna implementation can show up as churn, support tickets, or higher data retransmissions—even when coverage is nominally sufficient. The antenna market’s growth reinforces the need for joint troubleshooting playbooks that span device, antenna and network layers.

A scaling story, not a hype cycle

Berg Insight’s 2025 shipment figure does not claim a new standard or a breakthrough feature. Its value is more practical: it quantifies the extent to which cellular IoT has entered a manufacturing-driven phase where components like antennas must be treated as scale-critical. For professionals building connected products, the message is straightforward—cellular IoT is no longer only about picking the right modem and tariff. It’s about executing the full RF-to-manufacturing stack reliably, at volumes that leave little room for rework.

The post Cellular IoT antenna shipments hit 757m units in 2025, signalling a new scaling phase for device hardware appeared first on IoT Business News.