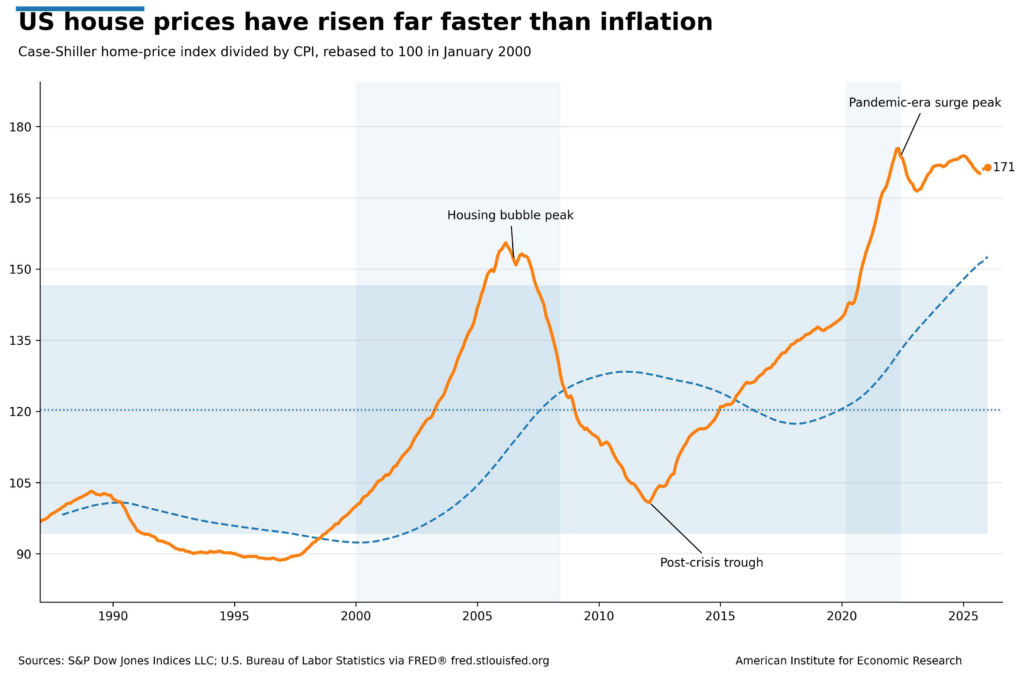

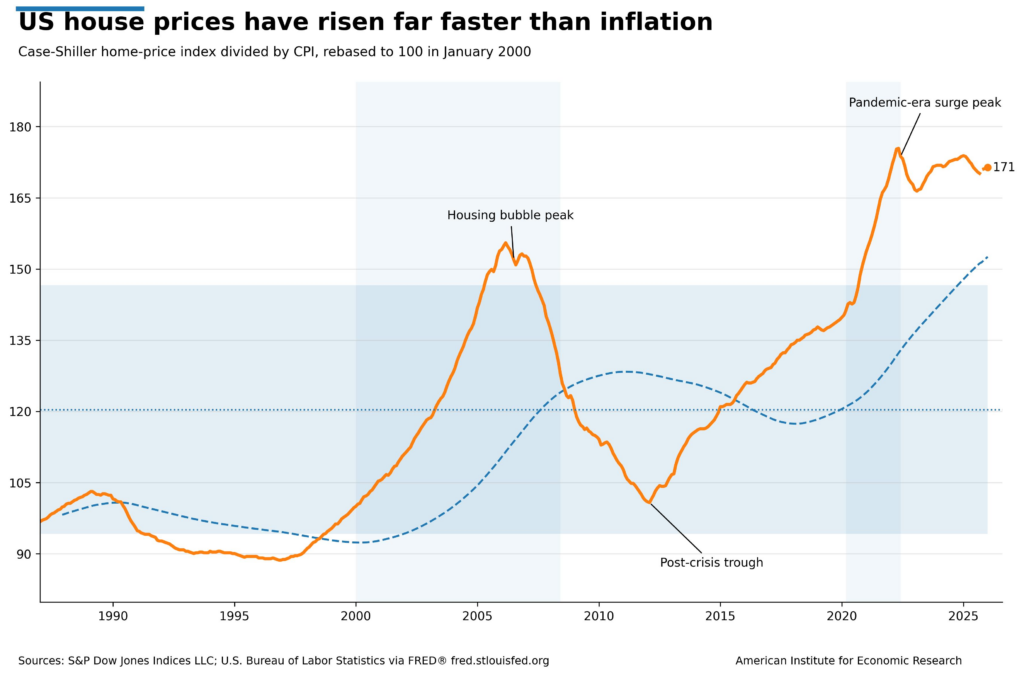

Housing affordability might be the defining economic crisis facing Americans today. Prices have surged in recent years, and the country is short millions of homes.

There are both obvious and subtle harms created by the housing shortage. When housing prices rise (as compared to incomes) people have less money left over for other goods and services. Others might be unable to afford housing at all, increasing homelessness. Productivity slows because workers find it difficult to afford living in high-productivity cities. And fertility rates often fall as high housing costs cause families to put off or, even avoid, having children.

Naturally, people are looking to hold someone responsible for the high cost of housing. Increasingly, both the left and the right are placing blame on institutional investors — private equity firms and large corporations that buy residential properties. The Senate recently voted to advance the 21st Century Road to Housing Act, which would, among other things, ban institutional investors from buying single-family homes.

At first glance, the argument that institutional investors are to blame for the housing crisis has intuitive appeal. Large corporations can bid up the price of housing, placing it out of reach of ordinary American families. Consequently, families who may otherwise have bought a home will turn to renting or informal arrangements.

At second glance, however, it becomes clear that this diagnosis of the housing shortage is inaccurate. Most notably, institutional investors simply do not account for most home purchases; they account for between one and two percent of the nation’s single-family housing stock and roughly three percent of single-family rental properties. In most markets, the overwhelming majority of homes are still bought by individuals. Even in dense metropolitan areas where corporate ownership has grown, institutional investors represent no more than three percent of homes in any housing market.

Plus, there are material advantages to renting compared to buying a home. When you rent, you have the flexibility to move for a better job without worrying about selling into a bad market, avoiding the costs of a massive down payment and ongoing repairs. You also don’t have to tie up a lot of wealth in a single asset whose value depends on one neighborhood and one local market.

But the core objection to banning institutional investors is that it does nothing to address the deeper problem: the lack of sufficient homes to meet demand. To understand why we don’t have enough homes, it helps to step back and think about how markets normally work.

Suppose demand for bread suddenly surges. Maybe a city’s population grows quickly, or a new gluten-heavy diet sweeps the nation. Whatever the reason, people are buying more bread than before. As a result, the price of bread rises. In turn, profit-driven bakers realize that there’s a lot of money to be made by baking more. So they produce more bread, pushing its price back down.

Rising prices encourage producers to produce more of a good, eventually making it more affordable. This is well-known. So why aren’t we seeing this play out in the housing market? If lots of people want to live in a particular city — say, because the jobs pay well or the schools are good — housing prices will initially rise. But you’d expect those higher prices to incentivize developers to build more housing, just as higher bread prices incentivize bakers to bake more bread. As more housing is built, the increase in supply should bring prices back down.

The reason why we don’t see developers building more housing in response to higher prices isn’t because they’re not interested in making more money. Rather, it’s because their ability to build is heavily restricted in much of the United States. For instance, large portions of many cities are zoned exclusively for single-family homes. Apartment buildings are prohibited in areas where developers might want to build them. Even when building is permitted, lengthy approval processes can delay projects for years. In San Francisco, it takes an average of 523 days to secure permits for a housing project. In New York, a lawsuit challenging the 2018 Inwood rezoning — intended to allow roughly 1,800 new housing units — held up the first project in the area for approximately three years before it was able to secure final approvals. And height limits, parking requirements, and other regulations can also make construction prohibitively expensive. Recent analysis estimates compliance and fees comprise 24 percent of new home prices.

In short, the root of the problem isn’t primarily increased demand for housing, though demand pressure is present. Rather, the problem is government-imposed restrictions that make it difficult, if not impossible, to adequately increase supply in response. Consequently, prices rise and stay high. Even if every institutional investor disappeared tomorrow, the housing shortage would remain.

So why do institutional investors take the blame for the housing crisis if they’re not the ones responsible? One possibility is that it’s simply easier to fault a visible, identifiable actor than a set of impersonal and poorly designed rules.

“The reason so many people misunderstand so many issues is not that these issues are so complex,” wrote the maverick economist Thomas Sowell, “but that people do not want a factual or analytical explanation that leaves them emotionally unsatisfied. They want villains to hate and heroes to cheer, and they don’t want explanations that fail to give them that.”

When people see harm being done, they want to blame someone for doing it. Large institutional investors are concrete agents, easy to name and criticize, whereas zoning restrictions and permitting delays are more diffuse and intangible.

At the same time, there’s a powerful intuition that it’s unfair that institutional investors can buy residential properties. It seems wrong that large corporations can outcompete ordinary buyers for homes. But this intuition is misleading. In a well-functioning market, being outbid by a wealthier buyer is not itself a problem, because supply expands in response. (A billionaire could easily outbid me for a particular loaf of bread, but that’s fine because he’ll induce bakers to bake more). The real issue in housing is not that some buyers have deeper pockets, but that the market is constrained in ways that prevent new supply from being built (bread being baked) when demand rises.

On the bright side, the solution is clear enough: make it easier to build more housing. Government officials should relax zoning restrictions that prohibit high-density housing and simplify approval processes that can delay projects for years. If these reforms were to happen, the same basic mechanism that works to reduce prices in countless other markets will work in housing as well. Until we remove the barriers that prevent builders from building, housing will remain unaffordable. Banning institutional investors might feel satisfying, but it won’t do much good.