Berg Insight forecasts the active installed base of video telematics systems in North America and Europe to reach about 22 million units by 2030, underscoring how quickly camera-led safety and operations tools are becoming mainstream in commercial fleets.

Fleet telematics has long been about location, engine data and compliance. What’s changed in the last few years is that video has moved from a niche add-on to a primary interface for safety, incident management and driver coaching—often shaping how fleets select platforms in the first place. Cameras generate operational evidence, not just telemetry, and that shifts buying decisions toward vendors that can manage high-volume data flows, retention policies and workflow automation at scale.

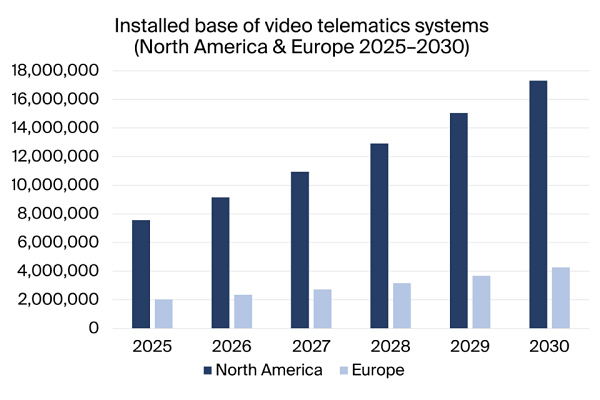

That context matters for Berg Insight’s latest video telematics study, which puts hard numbers behind the trend. The firm estimates the active installed base in North America reached almost 7.6 million units in 2025, and forecasts it will grow at a CAGR of 18.0 percent to exceed 17.3 million units by 2030. In Europe, the installed base is estimated at over 2.0 million units in 2025 and is projected to grow at a 16.0 percent CAGR to reach 4.3 million units by 2030.

Put together, those forecasts imply an installed base of roughly 21.6 million active systems across the two regions by 2030—effectively the “22 million” headline figure. The scale is important: video telematics is no longer an emerging category; it is becoming a core fleet technology layer that vendors must support operationally, commercially and technically.

A market that’s growing fast—but not evenly

Berg Insight characterises North America as the frontrunning market, more than three times the size of Europe, where activity has so far been largely dominated by the UK. This regional imbalance is one of the most consequential takeaways for IoT and telematics professionals because it shapes product strategy and channel economics.

A concrete implication of Berg’s numbers is that most incremental units through 2030 will be deployed in North America, where the installed base is forecast to add close to 10 million active systems from 2025 to 2030. For vendors and integrators, that typically means prioritising integrations, installer capacity and support operations in that region—even if Europe is growing quickly in percentage terms.

Not just “more cameras”: convergence is the real differentiator

Many market updates treat video telematics as a straightforward camera rollout story. Berg Insight’s framing makes a more specific point: video telematics spans standalone camera-based applications as well as extensions to conventional telematics, and an increasing share of providers now deliver “all-in-one solutions integrating fleet and video telematics capabilities on the same platform,” according to Rickard Andersson, Principal Analyst at Berg Insight.

That platform convergence is what makes this announcement distinct from typical growth forecasts. It suggests the competitive battleground is shifting away from isolated camera hardware and toward unified platforms where video, sensor data and fleet workflows live together. For enterprise fleets, a combined platform can reduce operational fragmentation—fewer dashboards, fewer integration projects, and clearer chains of custody for incident evidence. For suppliers, the convergence raises the bar on backend architecture, data governance and lifecycle management, because video introduces different storage, connectivity and privacy considerations than classic telematics telemetry.

How Berg Insight segments leadership

The study also maps a competitive landscape that cuts across three types of players: video telematics specialists; general fleet telematics providers that have added video; and hardware-focused suppliers selling mobile DVRs and vehicle cameras used for video telematics.

Berg Insight ranks Streamax, Samsara and Lytx as leading players in their respective categories. Streamax is positioned as the leading hardware provider, and Berg Insight notes it has equipped more than 5 million commercial vehicles globally to date, while also offering software platforms and subscription services widely used with its hardware. In the general telematics camp, Samsara is highlighted as a front-running video solution provider with the largest number of camera units deployed across its subscriber base. Lytx is described as the largest video telematics solution specialist and the first to surpass 1 million vehicle subscriptions for video telematics specifically.

Berg Insight also points to other significant players with estimated installed bases of around half a million units or more, including Motive (formerly KeepTruckin), Howen, Netradyne and the channel-focused brand Xirgo (formerly Sensata INSIGHTS, including the acquired video telematics company SmartWitness). The remaining top-10 players are named as VisionTrack, LightMetrics and Nauto.

What it means for OEMs, SIs and connectivity providers

For OEMs and upfitters, the growth trajectory implies video is becoming a default requirement in commercial vehicle digital packages, not a premium option—especially in North America. System integrators will likely see more demand for projects that unify camera deployments with existing fleet telematics platforms rather than rip-and-replace programs.

Connectivity providers, meanwhile, should read the forecast as a signal that the “cost per connected vehicle” conversation is evolving. Video systems typically drive different data usage patterns and service expectations than GNSS-plus-CAN deployments, which can influence SIM management, policy controls and support models—even when vendors aim to minimise bandwidth with event-based uploads. The vendors that execute best may be those that make video operationally manageable at scale, not merely those that ship the most devices.

The post Video telematics is set to double in five years, with North America still dictating the pace appeared first on IoT Business News.