Compare this argument from President Trump on Truth Social, in January 2026, to another (perhaps the same?) made by Pierre Joseph Proudhon in 1849.

I protest against your credit at five per cent, because society is able and ought to give it to me at zero per cent; and, if it refuses to do so, I accuse it, as well as you, of robbery…

– Pierre Joseph Proudhon, Bastiat-Proudhon Letter #5, 1849.

Some arguments, we think, have been won decisively. Logic has forever buried their adversaries. And yet, friends of freedom find themselves defending free speech and the Enlightenment itself (in an age of old socialism and new post-liberalism). I never thought I would have to rediscover the nineteenth-century arguments of Frédéric Bastiat in favor of free trade. But here we are, in an age of tariff wars.

I thought Bastiat would remain a wise portrait looking down on interns and scholars in AIER’s library, or perhaps a gem to be shared with my undergraduates as a witty illustration of basic economics. But the politicians are back to their economic sophistry, so I find myself re-reading Bastiat.

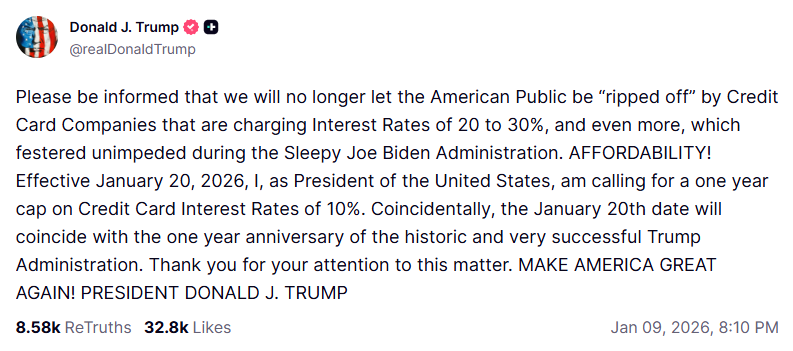

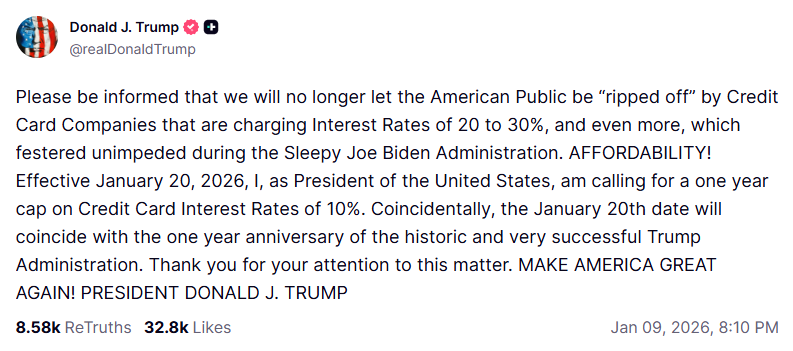

On January 10 of this year, President Trump posted a call for credit card interest rate caps of 10 percent, effective January 20. His announcement was not followed by an executive order, so the cap hasn’t been implemented (it would have been interesting to see what presidential authority he claimed, but that’s a different story).

Last year, Representative Ocasio-Cortez and Senator Bernie Sanders introduced bills proposing 10-percent caps on credit card interest rates. The bills are stalled in their respective chambers, but President Trump’s announcement has revived lobbyist interest in moving the bills forward.

This year, there’s another twist. Instead of a national 10 percent interest rate cap, the Empowering States’ Rights to Protect Consumers Act would allow each state to cap interest rates within its borders.

Interest rate caps are a bad idea (as are any price controls). My purpose here is not to explain why (John Phelan does so nicely in his recent column in these pages). Nor is it to explain the difficulties, economic and constitutional, with a hodgepodge of conflicting state-level regulations. Nor is my intention to worry about the effects of such short-sighted interventionism on the most vulnerable Americans.

Instead, I propose to take a walk down memory lane, by returning to the Bastiat-Proudhon debate on interest of 1849-1850.

The Bastiat-Proudhon Debate on Interest

The debate took place in the pages of La Voix du Peuple (“The People’s Voice”) between October 1849 and March 1850. It comprises a total of 14 letters.

Pierre Joseph Proudhon (1809-1865) was a French journalist, philosopher, and socialist. Proudhon favored peaceful social revolution, and called for a national bank to extend “free” credit. He is most remembered for coining the phrase “property is theft”.

Frédéric Bastiat (1801-1850) was a French lawyer, journalist, and economist. He is most remembered for his series of essays on “what is seen and what is not seen,” and his defense of free trade and limited government. A clever writer, Bastiat often used humor, as well as reductio ad absurdum, such as when he proposed banning sunlight (through mandatory curtains) to protect the candlemakers, and reducing the trade deficit by sinking ships returning with gold from export sales. He is most remembered for the broken window fallacy. Along with John Locke and FA Hayek, he presides over the learning in AIER’s library.

Bastiat argues that interest is compensation – both just and economically sound – for the forgone use of capital, but also for the service rendered by the loan of capital. Proudhon disagrees: capital is returned after the loan period, so any interest is mere exploitation. What is more, interest might once have been necessary to attract capital, but the economy is now sufficiently advanced that it can pool funds in a national bank and provide interest-free loans.

The Argument

Bastiat explains that a loan involves two parts (Letter 2): “1. the restoration, intact, at the expiration of the loan, of the object lent; 2. a service to be rendered the lender by the borrower as compensation for the service which the latter has received.”

Capital increases productivity, thus benefiting both the borrower and the economy as a whole. Bastiat argues that tools and capital can’t exploit workers, because by the borrowing of tools, the worker can produce much more than he could alone. So even if the lender of the tools claims some share of the greatly increased production, the worker is left better off than he would’ve been working only with his hands. “And because he surrenders to me, freely and voluntarily, one-twentieth of this surplus, you represent me as a tyrant and a robber,” Bastiat asks. “The workingman shall see his labor increase in productivity, humanity shall see the sphere of its opportunities enlarge, and I alone, the producer of these results, must be prohibited from participating in them, even by universal consent!”

Capital, writes Bastiat, “in the form of wheel, gear, rail, waterfall, weight, sail, oar, plough, performs so large a part of the work,” that it should be considered “the friend and benefactor of all, and especially of the suffering classes.” Laborers should celebrate capital, “desire its accumulation, its multiplication, its unlimited diffusion,” because it multiplies the efforts of “nerves and muscles” and increases the value of workers’ productive contributions.

Proudhon disagrees. He starts by claiming that the owner of capital wouldn’t lend it if he were using it, “does not deprive himself,” but “he lends it because he has no use for it himself.” Capital, by this argument, requires labor, and otherwise “this capital, sterile by nature, would remain sterile, whereas, by its loan and the resulting interest, it yields a profit which enables the Capitalist to live without working… a contradictory proposition.”

Bastiat counters that there is, in fact, an opportunity cost to lending, so the lender can command “a compensation for delay,” where the lender has forgone consumption. Interest on capital lent is, he says, “the price of time.” Real-world lending must also be priced to account for the risk of lost principal.

Proudhon then calls for a national bank, which could lend at zero interest. He proposes to finance this bank through a wealth tax. He continues:

a single tax should be established, not on production, circulation, consumption, habitation, etc., but, in accordance with the demands of Justice and the dictates of Economic Science, on the net capital falling to each individual. The Capitalist, losing by taxation as much as or more than he gains by Rent and Interest, would be obliged either to use his property himself or to sell it; economic equilibrium again would be established by this simple and moreover inevitable intervention of the treasury department.

To Proudhon, any interest is usury, because society owes him access to capital: “I protest against your credit at five percent, because society is able and ought to give it to me at zero percent; and, if it refuses to do so, I accuse it, as well as you, of robbery; I say that it is an accomplice, an abettor, an organizer of robbery.”

Bastiat counters with simple economic logic. Incentives matter. Without interest, there will be no capital to be lent: “in order that it may exist, it must have an incentive to birth in the prospect of reward offered to the virtues which create it.” Unless, he writes, “the time has come when houses, tools, and provisions spring into existence spontaneously,” then the capitalist is indeed laboring, and to continue to lend, will have to be compensated. If no one lends capital, productivity goes down, and prices go up. Indeed, by forgoing interest, we risk a “return to barbarism, to the time when a thousand days’ labor would not have procured a pair of stockings.”

Pretending that lending isn’t a necessary and productive activity is “to say that capital ought to vanish from the face of the earth, is to say that Peter, John, and James ought to procure their transportation, their wheat, and their books by the performance of as much labor as would be necessary to produce these things directly, and with no other resource than their hands.” Our escape from subsistence living owes much to what we might today call the Austrian structure of production: “All Capital… is the result of prior Labor, and increases the power of subsequent Labor. Inasmuch as it is the result of prior Labor, he who lends it receives a reward. Inasmuch as it increases the power of subsequent Labor, he who borrows it owes a reward.”

Interest Rate Caps Fail Every Time

Proudhon, in his debate with Bastiat, committed all the sins shared by socialists, from Marx to Zucman. His “economic theory” relies on wishful thinking, attempting to replace laws of economics with lofty sentiments and shoddy logic that falls apart under the simplest scrutiny.

Proudhon hoped his national bank would erase class conflict, despite its being funded by a tax on capital. Markets create spontaneous connections — economic harmonies — while nationalized capital lending would replace those natural balances of capital and labor with political agendas backed by force.

Bastiat’s theoretical foreshadowing is astonishing, but we also have concrete examples of his prescience. The Durbin Amendment to the Dodd-Frank Act of 2010 capped debit card fees. Banks responded by ending free checking account programs and raising account minimums and maintenance fees. The effect, far from increasing affordability, was to push a whopping one million Americans out of the banking system.

Almost two centuries after Bastiat made his case, the principle (and the principal!) remain the same. Interest rate caps were a bad idea then, and they’re a bad idea now, because they ignore the value that lenders contribute economically and make it less attractive to lend. That punishes those who need to borrow, and whose labor would be made wildly more valuable through alliance with capital.